Investing in times of inflation

Inflation can significantly impact investors. Now that we have laid the supposed “specter” to rest, this blog article will forge a link to the financial markets. How should investors be positioned in times of inflation? Find out which price index economists use to measure inflation and which asset classes and sectors have performed best in the past in an inflationary environment.

Economists differentiate between “headline inflation” and “core inflation”. Headline inflation includes

expenditures for volatile items such as food and energy. Core inflation, on the other hand, omits these short-term influences, and is viewed as an indicator of underlying long-term inflation.

In addition to differentiating between headline inflation and core inflation, investment experts also take into consideration differing types of price index when evaluating the effects of inflation. Here a comparison of the three most important ones—these are particularly relevant in the context of the US economy:

© Vontobel 2022. Source: Refinitiv Datastream, Vontobel.

In addition to actual inflation rates, investors are mainly interested in how their own portfolio can be optimized in times of rising or falling inflation. While past performance is no guarantee for future returns, we still think it makes sense to compare past trends for different asset classes and sectors.

For this purpose, we differentiate between three degrees* of inflation:

* In order to distinguish uniformly between inflation degrees in all markets, we classify them in accordance with US inflation. Calculation of yields below is based on global financial market data.

The following charts allow you to compare inflation effects in an environment of low, high and extreme inflation one after the other in the slider.

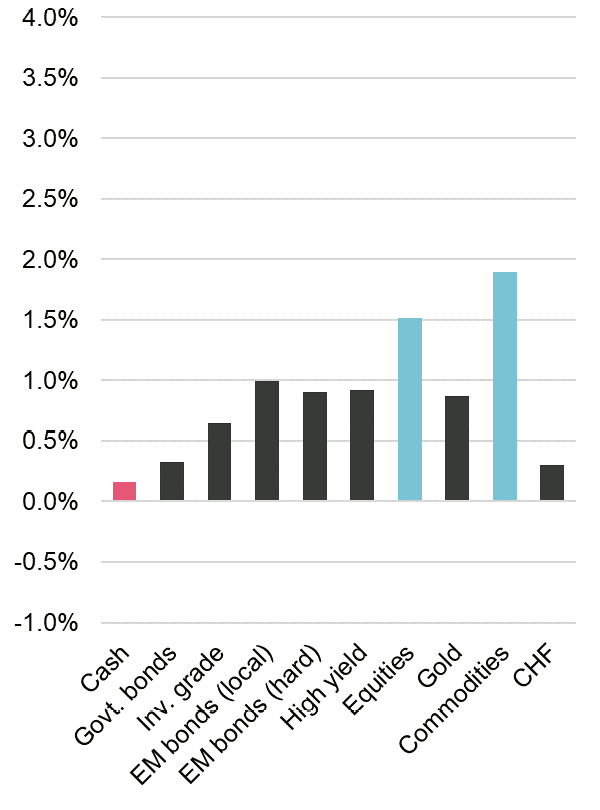

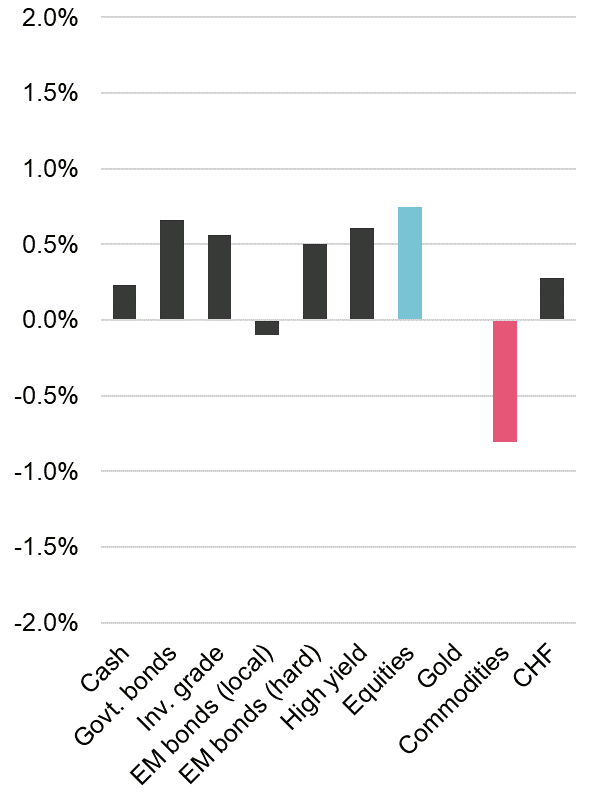

During times of rising, but low inflation, equities and commodities were the place to be, while cash was the least attractive option.

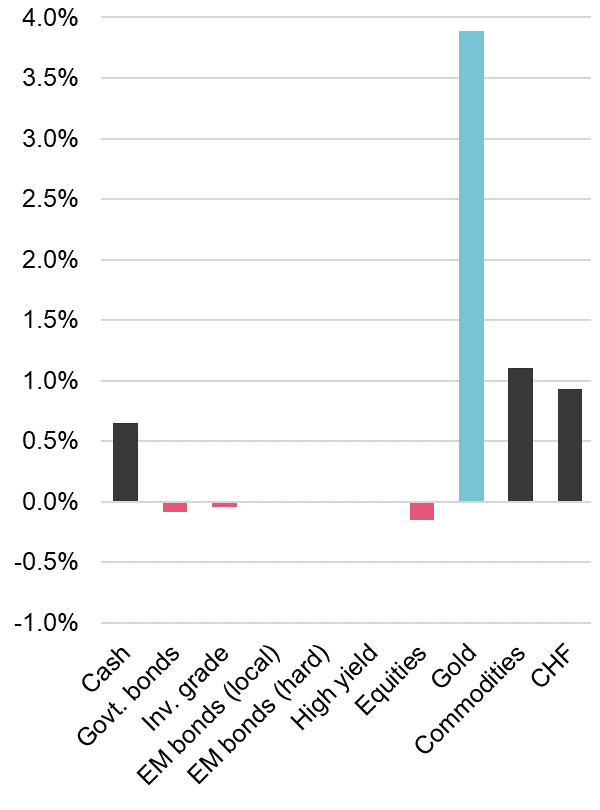

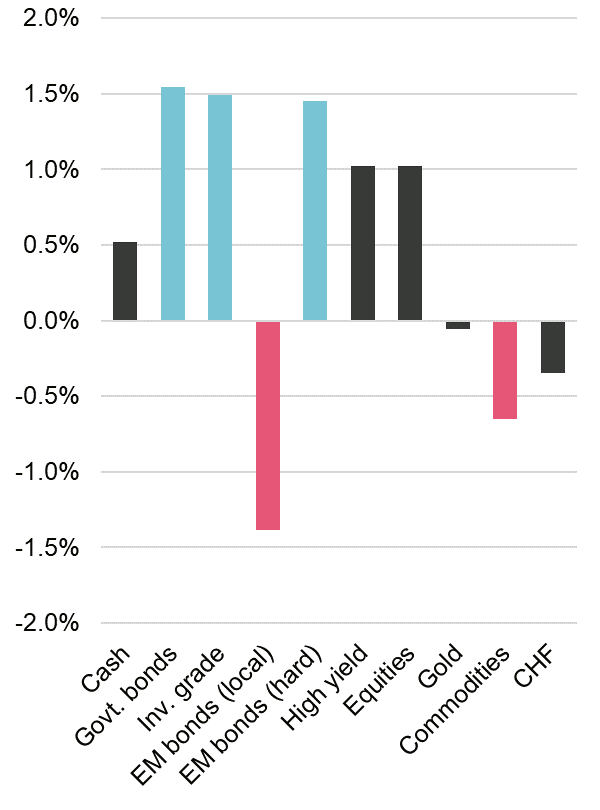

During times of rising, high inflation, investors have historically been well-advised to invest in commodities

and gold, but also equities posted positive returns.

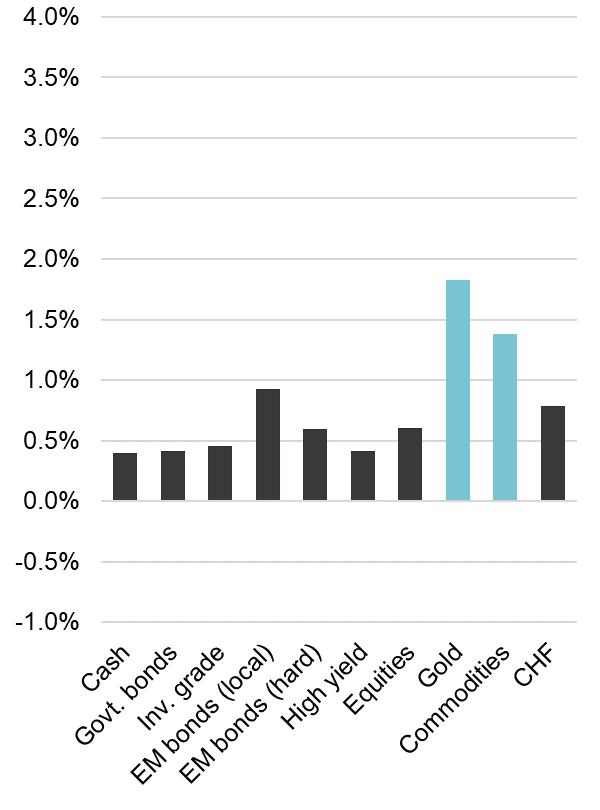

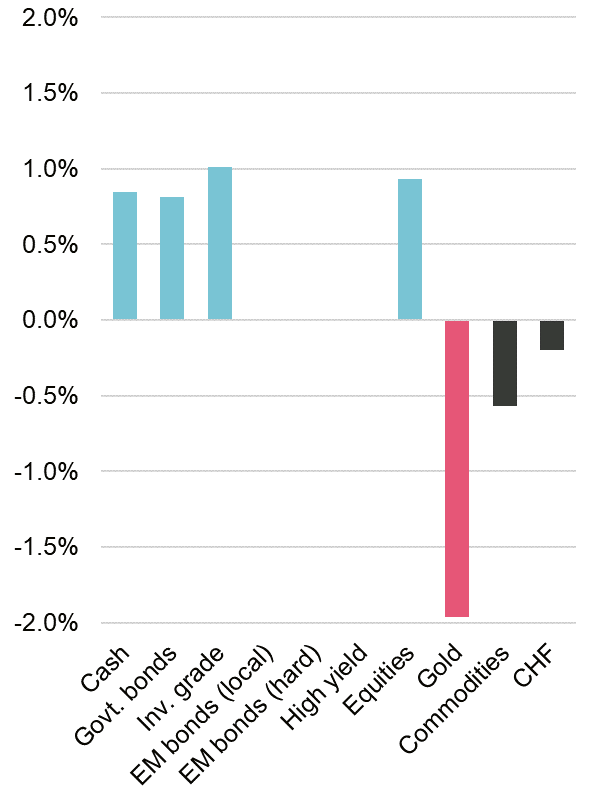

Lastly, the analysis suggests that gold seems to be the only place of shelter when inflation is spiraling

out of control (i.e., above 6 percent), while equities and longer duration bonds generated negative returns.

Source: Global Financial Data, Refinitiv Datastream, Vontobel.

Note: no data is available for EM local and hard currency bonds as well as high yield bonds during times of rising, very high inflation.

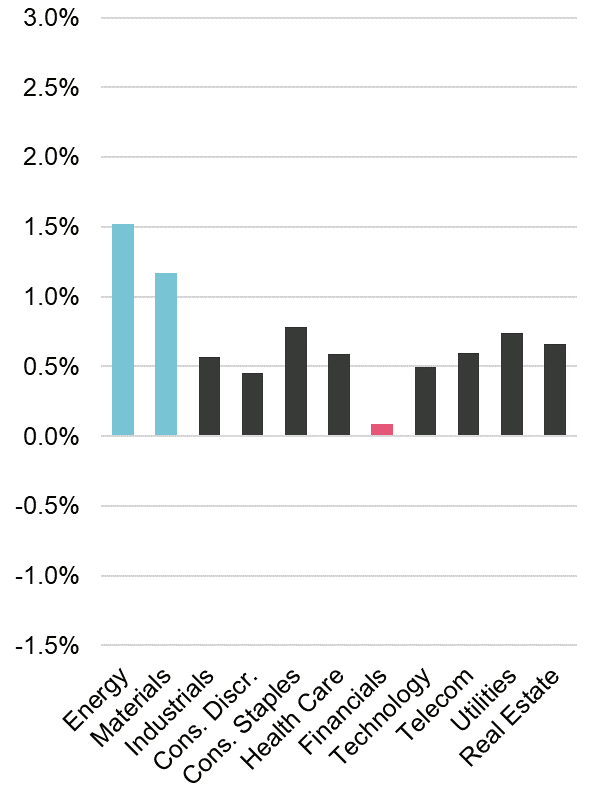

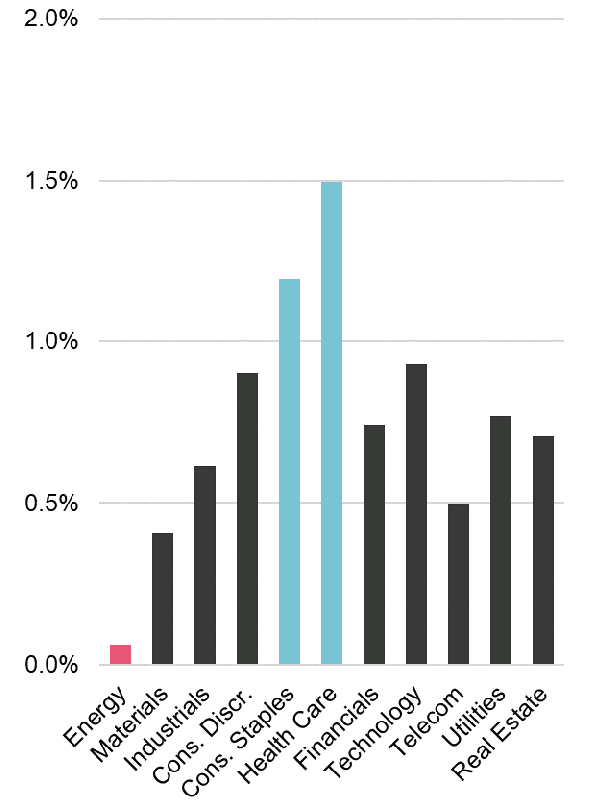

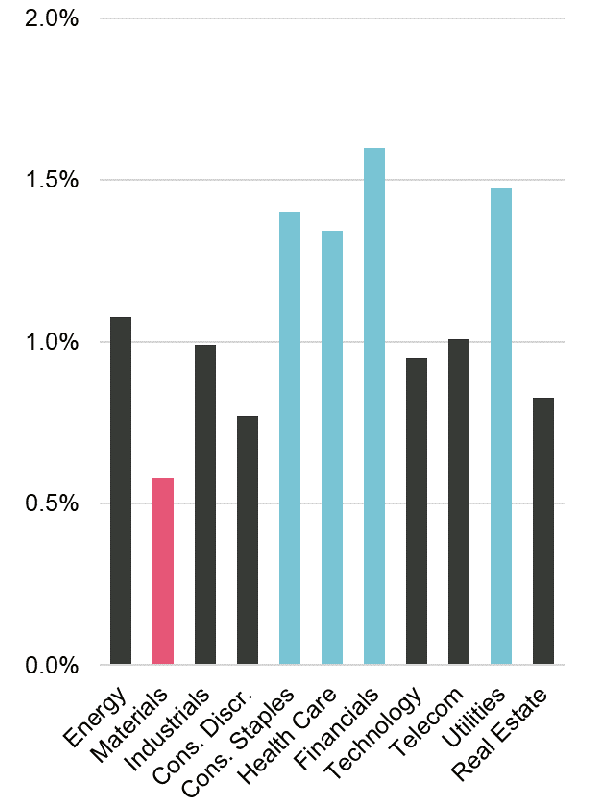

During periods of low inflation, tech managed to notch the highest returns while defensive sectors (consumer staples, health care, utilities) fared worst.

In a rising, high inflation environment, commodity sectors performed best and financials worst.

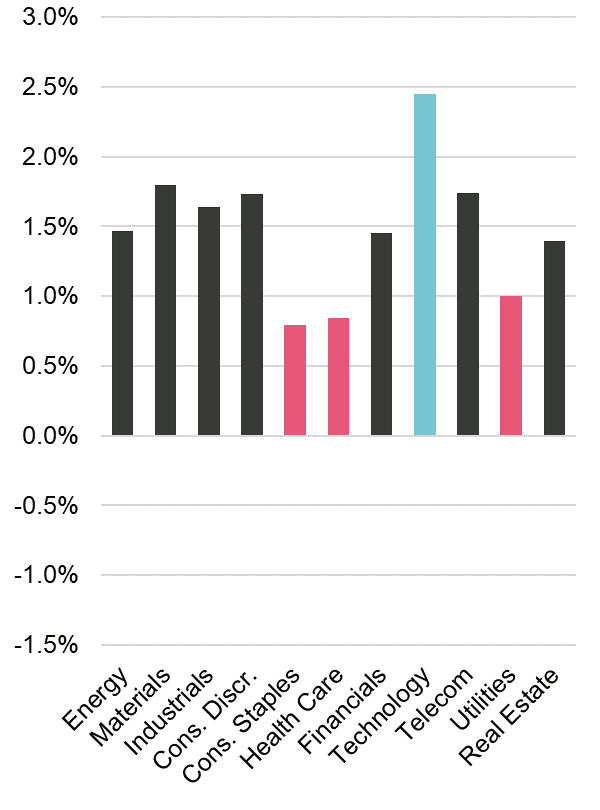

Commodity-related sectors also had the upper hand when inflation surged above 6 percent, while consumer-related sectors and tech were the least attractive.

Source: Refinitiv Datastream, Vontobel.

The chart demonstrates that in a low inflation environment, equities have performed best and commodities worst.

In a high inflation environment, assets with a long duration were best and commodities as well as emerging markets bonds in local currency worst.

In an environment in which prices came down from very high levels, cash, bonds, and equities fared best while investors were well-advised to stay away from gold.

Source: Global Financial Data, Refinitiv Datastream, Vontobel.

Note: no data is available for EM local and hard currency bonds as well as high yield bonds during times of rising, very high inflation.

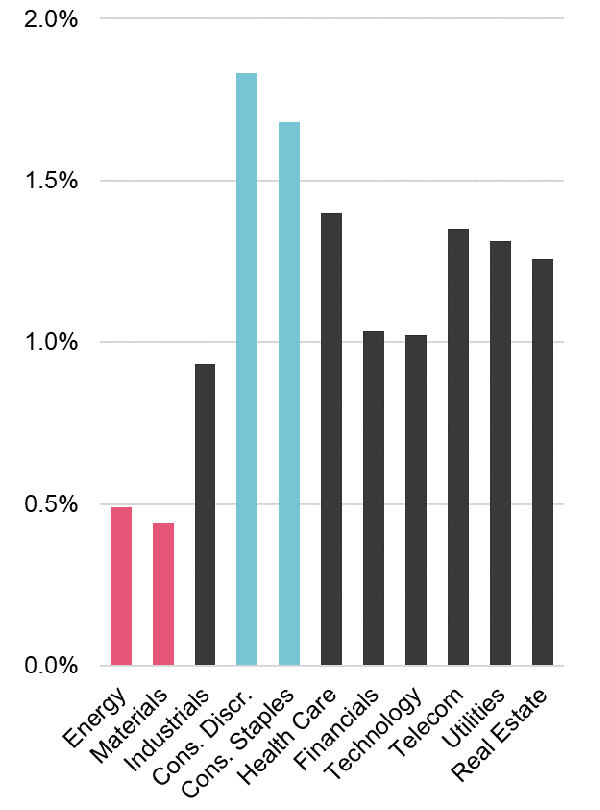

Health care and consumer staples performed best during times of falling and low inflation while energy struggled but was still positive.

Periods of high, but falling inflation benefited defensives and financials the most and materials the least.

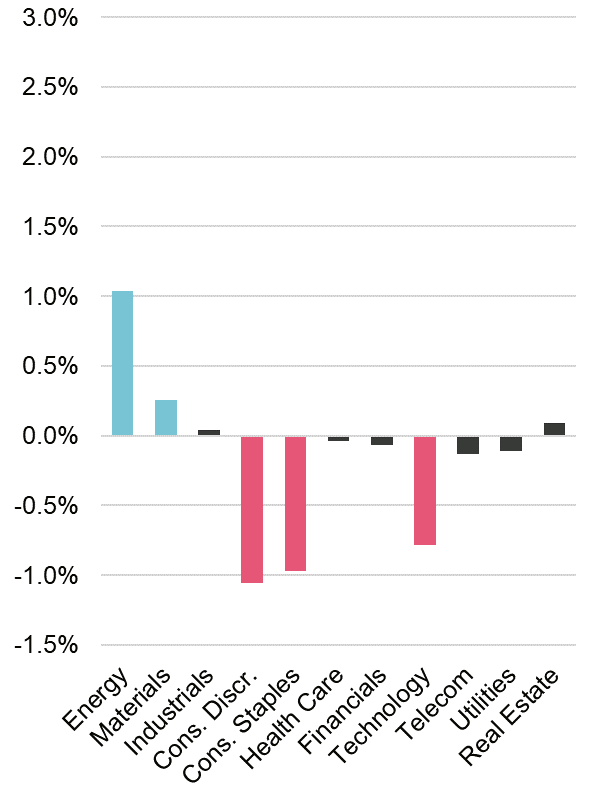

Periods of very high, but falling inflation bode very well for consumer-related sectors and not so well for commodity-related ones (see the chart below).

Source: Refinitiv Datastream, Vontobel.

Inflation can be a game-changer, especially when it is very high (i.e., exceeding six percent).

Commodities have historically lived up to their reputation as inflation hedges. While the asset class under-performs in normal times, it performs most reliably during times of rising inflation.

Our analysis shows that gold remains the best tail hedge for investors if inflation goes through the roof.

Our study also suggests that investors should not necessarily shy away from equities during times of rising prices: equities have mostly been able to withstand price pressure, even during periods of rising and high inflation. Our analysis indicates that the only time when exposure to stocks should have been reduced is when inflation was running out of check.

While equities do mostly well, a selective approach that fits with the inflation outlook is still key. This is especially true when looking at it from a sector perspective.

Markets seem to like such an environment – historically, most asset classes performed well, including cash, bonds, and equities.

The level of inflation seems to be less relevant when inflation falls than when it rises (in our analysis, bonds and equities performed only slightly better when inflation was falling, but above three percent).

Not very surprisingly, commodities tend to suffer when inflation comes down. The same is true for other inflation hedges, such as gold.

History has shown that the Swiss Franc has been depreciating versus the US-dollar in times of high but falling inflation – it is therefore not the place to be in such an environment.

In times of falling inflation investors should be selective with equities. Defensive sectors have historically outperformed during times of declining inflation. Also, financials have fared well, while commodity-related sectors should have been avoided.

En premier lieu les épargnants, car la hausse des prix diminue la valeur réelle de leur épargne.

L’inflation a également un impact négatif sur les salariés en contrat de travail à durée déterminée, ou sur les organismes de crédit tels que les banques qui ont accordé des prêts à taux fixe. Sans oublier les importateurs qui doivent généralement payer plus cher les biens importés lorsque la devise d’un pays ayant un taux d’inflation (national) plus élevé se déprécie face aux devises touchées par une inflation moindre.

En général, une hausse des prix profite à tous ceux qui ont contracté des emprunts assortis d’un taux d’intérêt nominal fixe: gouvernements, entreprises ou ménages.

De manière générale, les entreprises fortement endettées en bénéficient également car un environnement inflationniste leur permet souvent de répercuter la hausse des prix sur les consommateurs. «L’argent supplémentaire» qui en découle peut alors être utilisé pour le remboursement des dettes en cours.

Les particuliers qui ont investi dans des actifs servant de couverture contre l’inflation (valeurs réelles comme l’immobilier, les matières premières ou l’or) profitent eux aussi de l’inflation lorsque la valeur de leurs placements augmente.